Will you Actually be Able to Retire?

Key Takeaways:

- The cost of living will continuously go up every year. So once you retire and begin living off your retirement there is no more money coming in. And with inflation going up every year your spending power is being eroded, causing you to start drawing on the principle of what you have set aside, thus reducing your dividends and other payouts your investments have. Eventually you'll have to start working part-time again just to make ends meet.

- Saving for retirement needs to start with your first paycheck.

- Most people don't know what investments to make or what funds to participate in so they turn to financial advisors...

- Most companies offer some form of 401K or other programs

- One of the few products that Americans buy that they don't know the...

- Price, danger, risk

- The year the markets crashed (2008) Wall Street handed out $18B+ in bonuses to executives. What happened to the average joe?

- Across the board, actively managed mutual funds with higher annual fees do NOT outperform a simple market index with lower fees.

- A lot of fund managers actually hold index funds, they don't hold their own mutual fund products in their own portfolios.

Image is from Frontline PBS; The Retirement Gamble, September 21st, 2021

Robert Hilltonsmith's: The Retirement Savings Drain

- Robert Hiltonsmith (Contributor to the Documentary and Author of The Retirement Savings Drain (CLICK TO VIEW)

- He graduated with a masters in economics and began contributing regularly to his 401K

- Even in a relatively good market he would check his statement regularly and noticed it never seemed to go up other than by what he was contributing

- So he decided to check to see what funds (22 of them in total) he was invested in and how/why they were performing like they were

- He made a research project out of the curiousity

- The funds tell you next to nothing. They have names like "balance fund" or "growth fund." It's actually difficult trying to find out what the funds are actually invested in.

- In his research he noticed a metric called Exp. Ratio which he had to look up and realize it meant "fees." As he looked into fees further he began to discover all different kinds...

- Examples: Asset management, trading, marketing, record keeping, and administrative.

- The average actively managed mutual fund carries an Annual Expense Ratio of 1.3%. Some go up to 2% or even 5%.

- Let's assume you have have $50,000-$100,000 in your 401K and so you have to pay $500-$1,000 annually which doesn't seem like a lot but in the context of a 401K plan growing more and more every year with your contributions and compounded growth you end up paying well into the 6 figures over the course of the next 20, 30, or even 50 years. That's the difference between running out of money before you die or not having money to pass on to your heirs.

- The average family pays over $155,000 in fees over the course of their 401K lifetime.

Image is from Frontline PBS; The Retirement Gamble, September 21st, 2021

Image is from Frontline PBS; The Retirement Gamble, September 21st, 2021

Jack Bogle

- Founder of Vanguard; founder of a company that offers investment products with some of the lowest fees on the market.

- He says, "If you want to improve your retirement outlook you need to downsize Wall Street's Take."

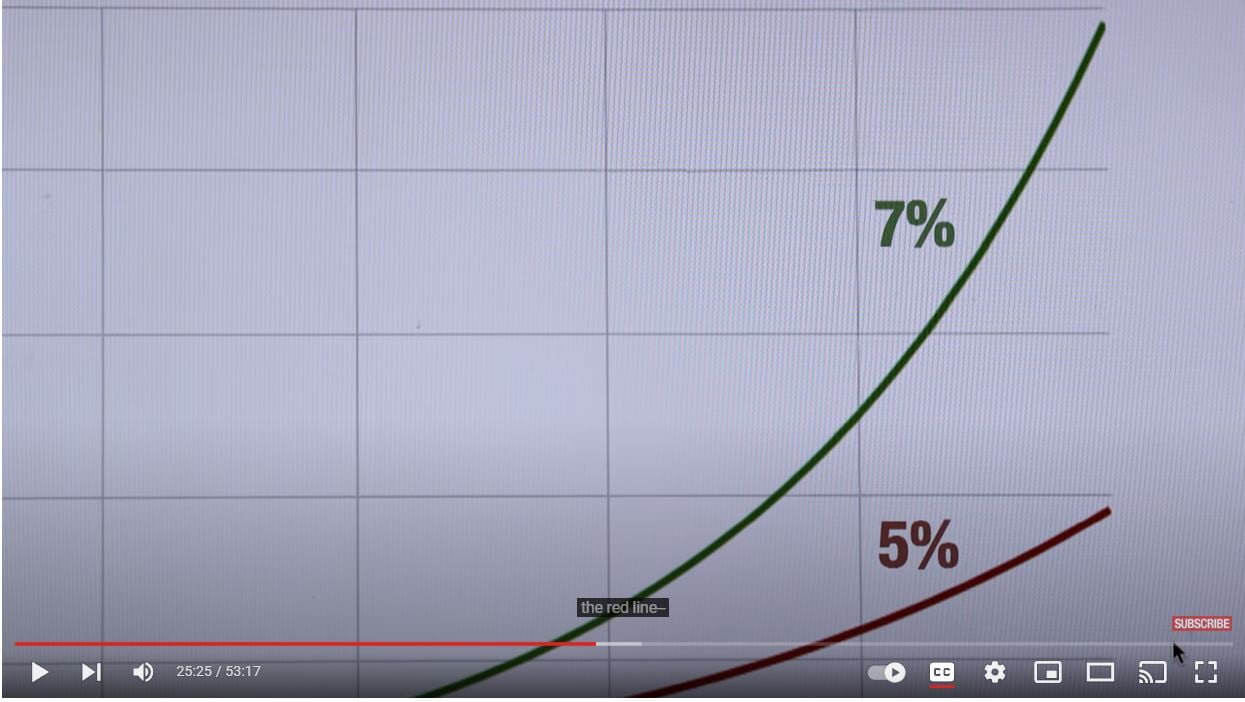

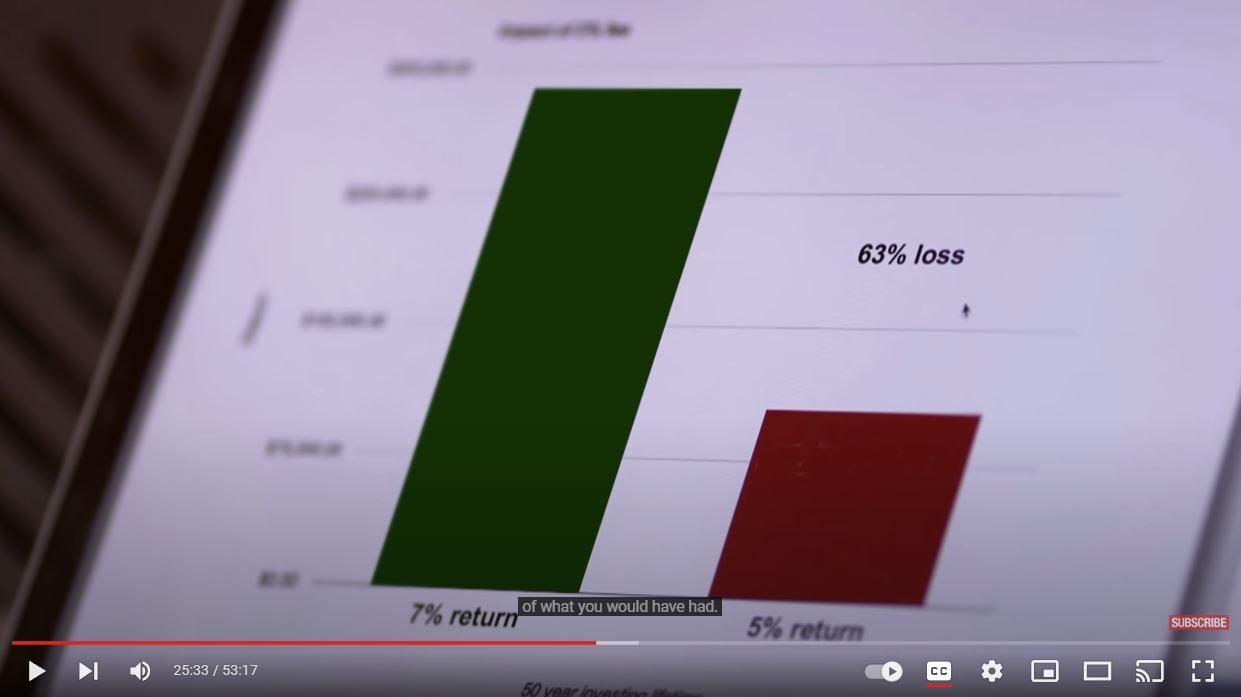

- Jack Bogle's example on the impact of fees...

- Assume you invest in a fund that averages an annual return on 7% for 50 years but charges you a 2% annual fee (so you only end up growing by 5%), the end result is staggering. You've lost almost 2/3 of what you would have hard (63% Loss).

- Do you really want to invest in a system where you put in 100% of the capital and take 100% of the risk but only take 30% of the reward you otherwise would have gained?

- Most people are unaware of the kind of fees they are paying. Most people just don't look at the fine print. There's confusing tables, with confusing names, and all sorts of different fees.

- Jack Bogle has been preaching Long-Term Index Funds for 40 years.

Get Wall Street out of the equation, get trading out of the equation, get management fees out of the equation. You own American Business and you hold it forever. That's what indexing is...own a fund that owns the entire US Stock Market, does no trading and has a cost of 1% a year to own. That is the only way to do it. Then you are a creature of the market and not of the casino.

If the math seems so simple then why don't most people just hold a diversified portfolio of long-term index funds?

- The fund industry has done a phenomenal job of marketing to the "busy" and "overworked" worker that doesn't have the time to learn and manage their own retirement so we will trust them.

- There are no CLEAR rules as to who can present themselves as an "expert." Anyone can present themselves a professional or an expert.

- The term financial advisor doesn't have any regulations or certifications that go with it.

- There is a term called a fiduciary and financial advisors that operate with that title are legally obligated to act in their client's best interest but not everyone utilizes that moniker and for those that do, how can you truly monitor all the potential decisions out there they didn't take and how do you know which one was in your best interest? In an uncertain market where even experts get it wrong sometimes how do you know your financial advisor's decision to buy/sell (x) was the best decision and if it wasn't did the broker still act with the best of intentions based on the information they had?

- Brokers typically try to sell the most profitable mutual funds. Brokers usually work on commissions for the funds that they sell.

- Some mutual funds have a surrender fee. On top of the 10% tax implications on early withdrawal before retirement age most mutual funds have a surrender fee which can even be an additional 10%. So if you lost your job and needed quick access to cash and decided to take $5,000 out to cover expenses for the next month or two you could lose $500 to the government and another $500 to the fund manager. So for every $5,000 you take out early you lose $1,000.